Double digit growth no more

May 24, 2023

The days of a double-digit annual growth rate for craft beer appear to be a thing of the past. That was the observation by Bart Watson, chief economist with the Brewers Association (BA).

Craft beer, which experienced double digit growth seemingly for decades, has now matured as an industry. Watson says slow growth is the new normal.

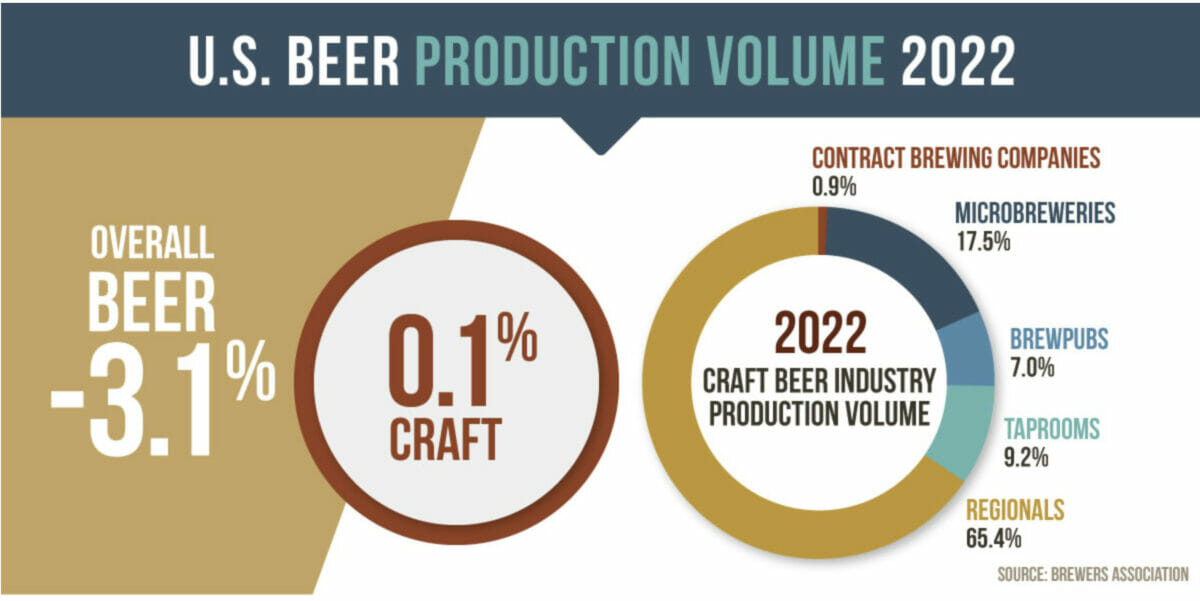

While traditional domestic beer (Bud-Miller-Coors-type beers) continued its steep decline of recent years, craft brewers have not fared nearly so poorly. Overall craft sales actually increased 0.1% in 2022. In fact, Watson projects, with the decline of traditional non-craft beer, craft brewers may provide the structure for new growth.

Dissecting the craft beer sector, one sees some parts doing better than others. Overall, hospitality brewers (taproom & brewpub brewers) are doing better than distribution-focused brewers. The following numbers compare 2022 to 2021.

Large craft brewery sales shrink a bit

Regional craft brewers suffered a business decline of 2%, year over year. Regional craft brewers have an annual beer production of between 15,000 and 6,000,000 barrels and comprise 65% of the craft market beer production. Regionals are large-size distribution breweries, which include many household names that reach back to the early days of craft. The category has not only suffered a loss of sales momentum from changing consumer preferences, but it also continues to lose members to acquisition by non-craft beer companies.

Microbrewers —the smaller category of distribution brewers—performed better, recording a 1% gain in sales. A few years back, these brewers were basking in double digit growth. Microbreweries are brewers that produce less than 15,000 barrels of beer per year and sell 75 percent or more of their beer off-site.

Among craft consumers, Watson says we are seeing a continued shift from distribution breweries to on-premise breweries.Watson predicts that 2023 will be a challenging year for distribution-focused brewers.

Hospitality brewers a bright spot

The bright spot among craft brewery categories were Taproom and Brewpubs — both breweries that focus on on-premise sales (with brewpubs more focused on full-service food offerings). These hospitality brewers recorded a growth rate of 7% in 2022 and were the healthiest part of the industry.

With over 9,000 locations, hospitality brewers are by far the largest category in numbers within the craft industry. Watson’s data shows that two-thirds of them are growing.

Watson says that within the hospitality category, one determining growth factor is innovation. The data shows that small brewers must innovate to stay competitive. Craft consumers are still in the mindset of wanting something new. As evidence of this preference, brewpubs opened after 2018 have a much stronger growth than those opened earlier.

Even with the maturing of the craft market, brewery survival rate is still much better than that for overall small businesses. It is still drawing lots of investment as a healthy number of new breweries continue to open. However, Watson predicts that this probably will not continue long term.

Draft Sales

For distribution brewers, draft beer sales are declining faster than their overall sales, meaning that packaged craft beer sales have become relatively more important for the larger craft brewers.

Across smaller craft brewers (taproom & brewpubs), draft beer sales are increasing and, in a sense, are supplanting a portion of draft sales from the larger craft brands. This trend of consumers preferring smaller, local breweries continues to affect the market.

Market challenges — Opportunities for growth

To continue its growth, Watson said the industry needs to find new opportunities and new places to sell craft beer. They need to create new demand by broadening craft beer outlets and audiences.

He says brewers should not focus so much on chasing style trends, but instead, focus more on what you do best and put more production emphasis there.

The new/upcoming generation of drinkers are not drinking craft as much as they are drinking other alcohol — especially cocktails. This is a challenge to craft beer. One way to combat that is by attracting and welcoming broader demographics to craft beer. Studies show that females and Black, Asian, and Latin alcohol consumers are still very under represented among craft beer consumers. Focusing more on how to include them gives craft brewers an opportunity for growth.

Chief Economist

Brewers Association

Watson spoke recently at the Craft Brewers Conference held in Nashville

BA Definition of Craft Brewer

The Brewers Association uses the following definition of craft brewer, which is used in reporting the statistics shown above.

Craft brewers are defined as small, independent brewers. They have an annual production of 6 million barrels of beer or less (approximately 3 percent of U.S. annual sales). Beer production is attributed to a brewer according to rules of alternating proprietorships. Less than 25 percent of the craft brewery is owned or controlled (or equivalent economic interest) by a beverage alcohol industry member that is not itself a craft brewer. The craft brewer has a TTB Brewer’s Notice and makes beer. The BA defines six distinct craft beer industry market segments: microbreweries, brewpubs, taproom breweries, regional breweries, contract brewing companies, and alternating proprietors.